Objective

ESPP and RSU is not part of Gensen Chousuu (Withholding tax / 源泉徴収) hence you’ll need to prep the information and declare yourself at time of tax return.

This article will desribe how to prepare tax info for ESPP and RSU.

Btw I’ve been asked before by a Tax Office to provide written evidence on inserted ESPP and RSU detail. How I prepared the evidence is described in this post.

Background Info

W-8BEN

W-8BEN is statement to prove you are paying tax in foreign country.

It is required to avoid double taxation.

Check your profile in Broker to determine if you’ve already made declaration for W-8BEN.

Contact to Broker if you are unsure on where to look for this info.

TTM, TTB, TTS

TTM, TTB, TTS each represents exchange rate.

TTS is generally used when cash flows from Yen to Dollar.

TTB is generally used when cash flows from Dollar to Yen.

TTM is the median of TTB and TTS.

Mizuho Website is very handy in identifying the rates for each day.

Comprehensive taxation (総合課税)

Comprehensive tax is idea of aggregating all income taxes.

Income Tax Rate varies depending on the aggregated amount.

Income Tax Rate can be found in Japan Tax Agency’s website

Resident Tax Rate is fixed to 10%.

Separate taxation (分離課税)

Separate tax is idea of calculation the income tax independently.

Only certain types of Income Tax is applicable for Separate taxation.

Income Tax Rate is fixed to 15.315%.

Resident Tax Rate is fixed to 5%.

Generally Separate tax is advantageous compared to Comprehensive tax unless your income is lower than 1,950,000 yen.

Average Acquisition Unit Cost (取得費の平均 / 総平均法)

If you’ve acquired share multiple times, whenever selling that share, instead of using individual Acquisition Cost, it is required by law to instead use the calculated “Average Acquisition Unit Cost”.

Eg,

Lets say you’ve purchased 5000 share at price of 800 yen.

Later you’ve purchased another 2000 share at price of 850 yen.

The next day, you’ve sold 3000 share at price of 900 yen.

Your “Average Acquisition Unit Cost” becomes ((5000 * 800) + (2000 * 850)) / (5000 + 2000), which is 815 yen (rounding up).

You will use this “Average Acquisition Unit Cost” to calculate the Acquisition Cost for the share you’ve sold.

815 * 3000 = 2,445,000

More desciption and example in Google and Japan Tax Agency website: https://www.nta.go.jp/taxes/shiraberu/taxanswer/shotoku/1466.htm

ESPP

Discounted Purchase

When share got purchased by ESPP, you need to declare the discount benefit as Income Tax (給与所得 / Comprehensive taxation).

Formula to calculate:

Eg,

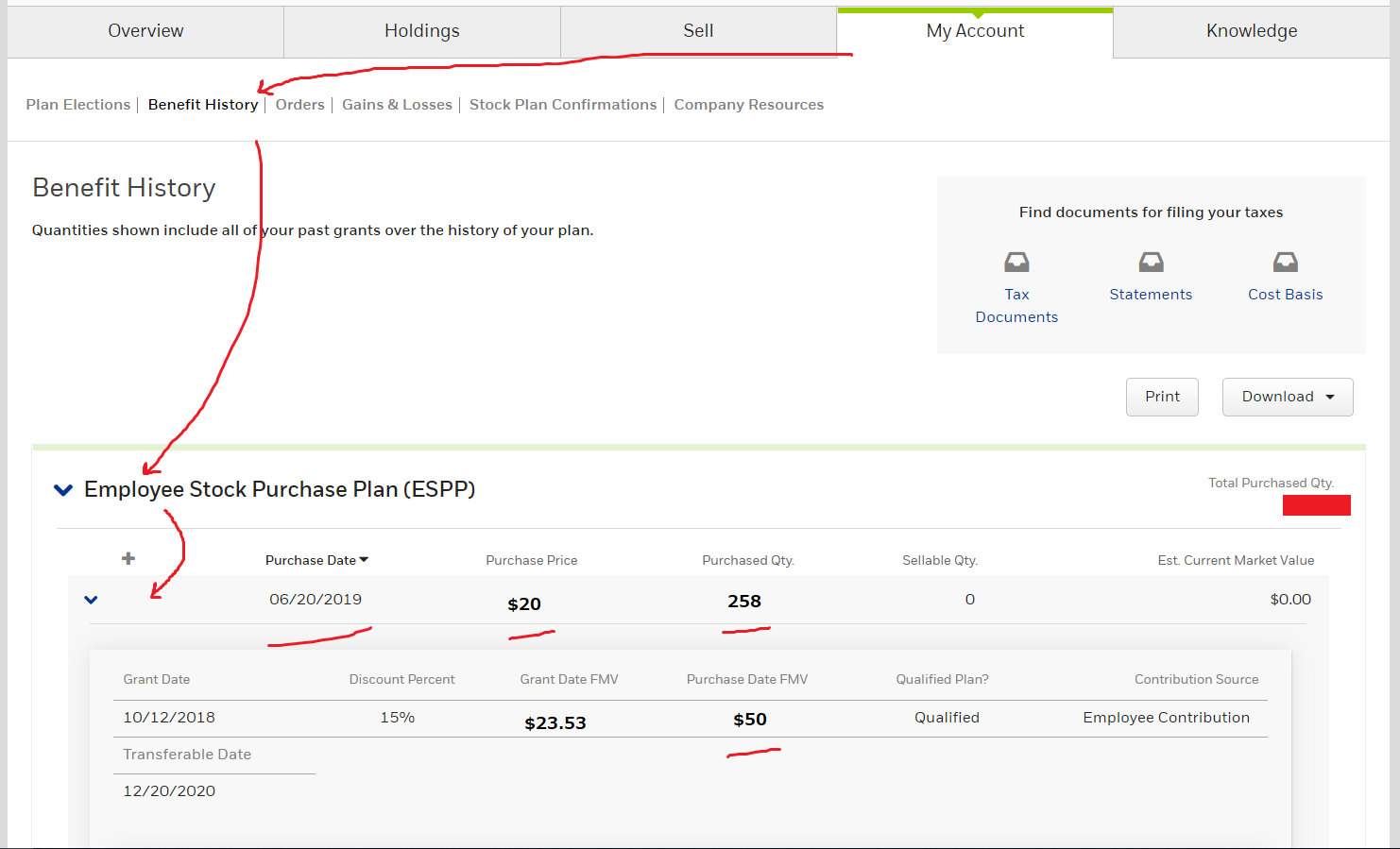

For etrade, find the necessary values from the “Benefit History” page

Substitute above values and formula will look like below:

Share Sold

Whenever you sell your share, you’ll need to declare capital gain or loss (譲渡所得 / Separate taxation).

Formula to calculate:

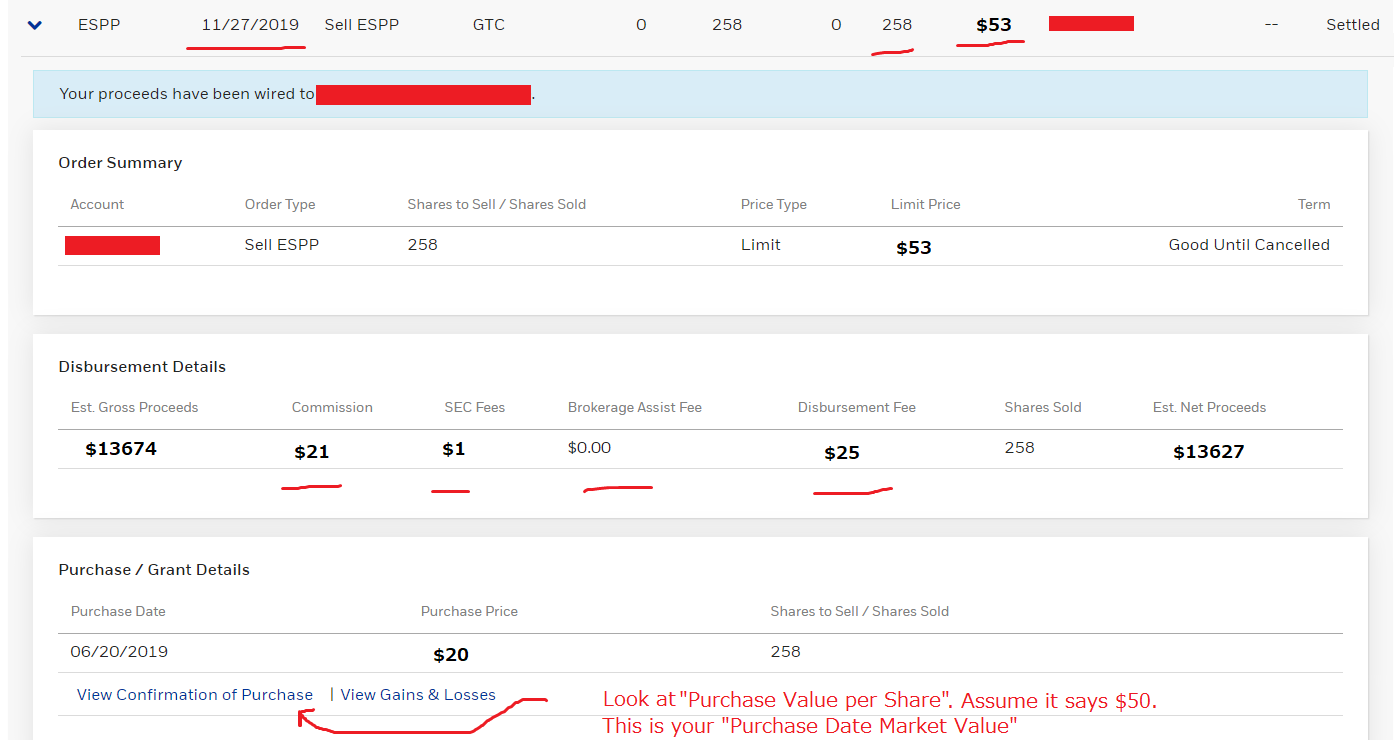

Acquisition Cost = Quantity * “Purchase Date Market Value” * “TTS when purchased”

Expenses = “Any Expenses” * “TTS when paid”

Eg,

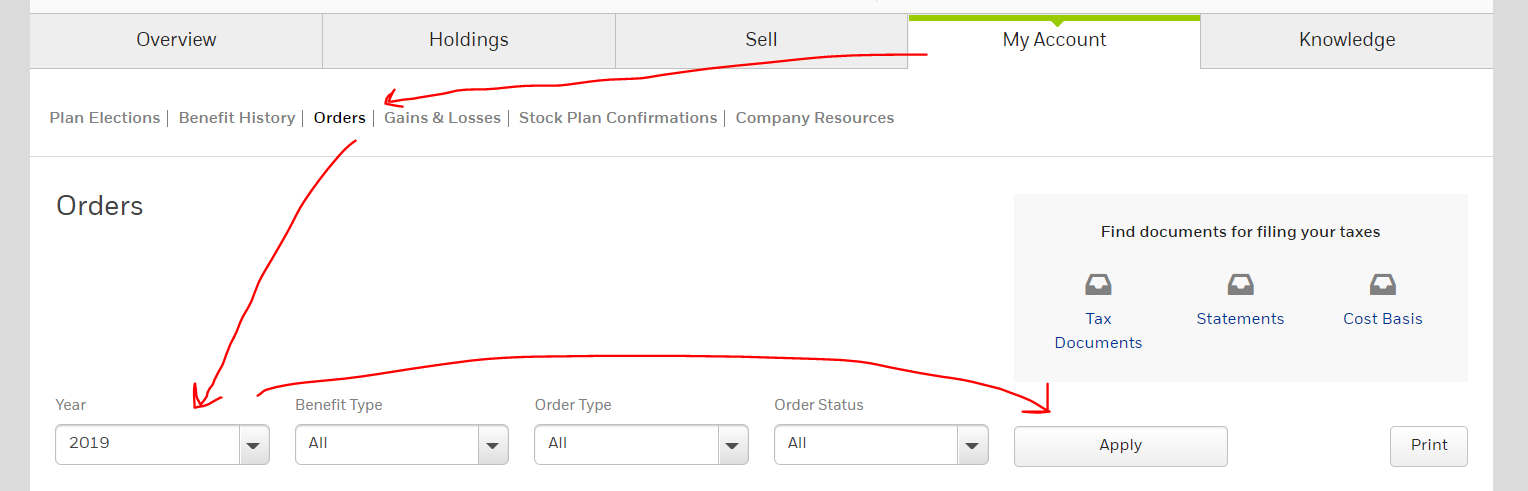

Open Orders page in etrade.

Expand the transaction

“Purchase Date Market Value” can be found in “View Confirmation of Purchase”.

Substitute above values and formula will look like below:

Acquisition Cost = 258 * 50 * 108.80

Expenses = (21 + 1 + 0 + 25) * 110.15

Dividend

Dividend must be declares as Dividend Income (配当所得 / Can be either Comprehensive taxation or Separate taxation).

My company does not provide dividend however I assume you’ll follow same procedure as dividend from Japan Company to declare it.

https://www.nta.go.jp/taxes/shiraberu/taxanswer/shotoku/1330.htm

Formula to calculate:

Note:

- If tax is auto deducted from Dividend, you will be eligible for “Foreign tax deduction” (外国税額控除)

- You are not eligible for “Dividend deduction” (配当控除)

Now since you are not eligible for “Dividend deduction”, it is beneficial to declare it as “Separate taxation” unless your total income is lower than 1,950,000 yen.

RSU

Vested

Whenever RSU is Vested (not Granted!), you pay tax.

The share you received have to be declared against Income Tax (給与所得 / Comprehensive taxation).

Formula to calculate:

Eg,

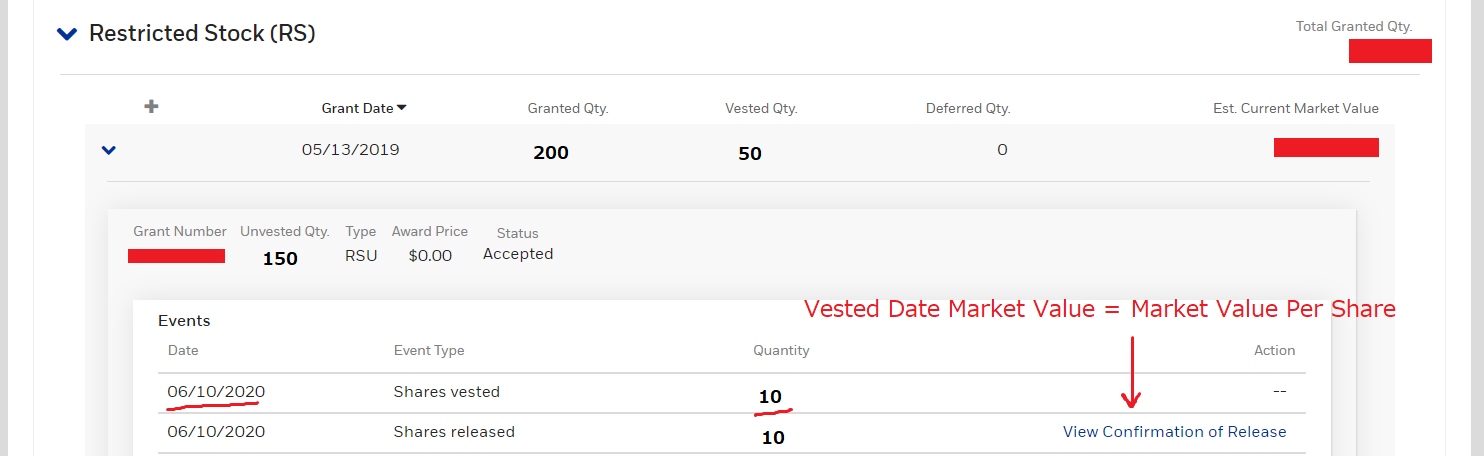

Open Benefit History page in etrade and navigate to section “Restricted Stock”

“Vested Date Market Value” can be found in “View Confirmation of Release”.

“Market Value Per Share” is your “Vested Date Market Value”.

Share Sold

Whenever you sell your share, you’ll need to declare capital gain or loss (譲渡所得 / Separate taxation).

Formula is similar to the one in ESPP:

Acquisition Cost = Quantity * “Vested Date Market Value” * “TTS when Vested”

Expenses = “Any Expenses” * “TTS when paid”

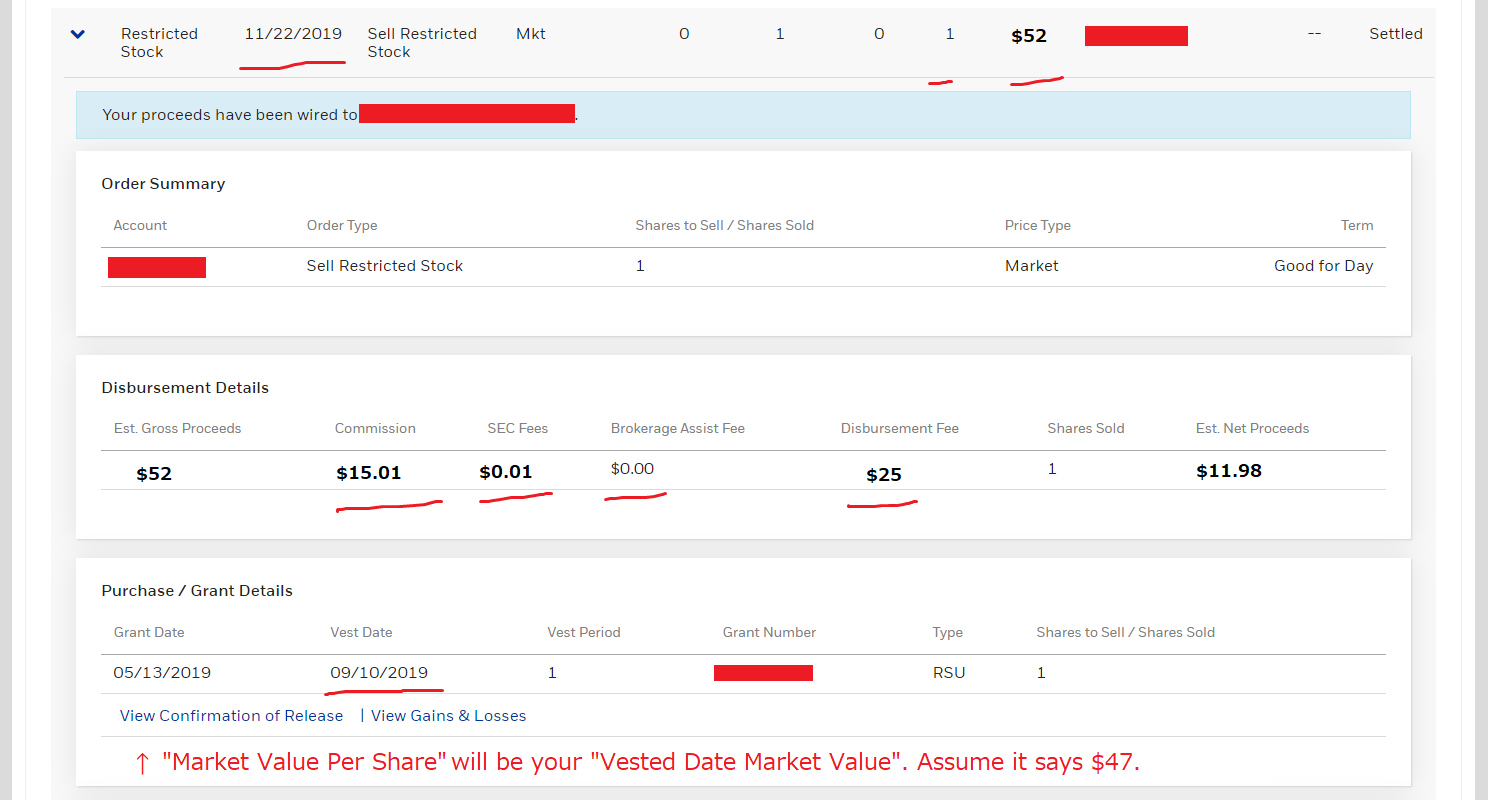

Eg,

Open Orders page in etrade and expand transaction for RSU.

上の画像だと下のような式になる:

Acquisition Cost = 1 * 47 * 108.45

Expenses = (15.01 + 0.01 + 0 + 25) * 109.69

Dividend

Dividend must be declares as Dividend Income (配当所得 / Can be either Comprehensive taxation or Separate taxation).

Same detail to one in ESPP.

Inserting to Kakutei Sinkoku (確定申告)

https://www.nta.go.jp/taxes/shiraberu/shinkoku/kakutei.htm

Open above link and start building Tax Return Document (確定申告書) online.

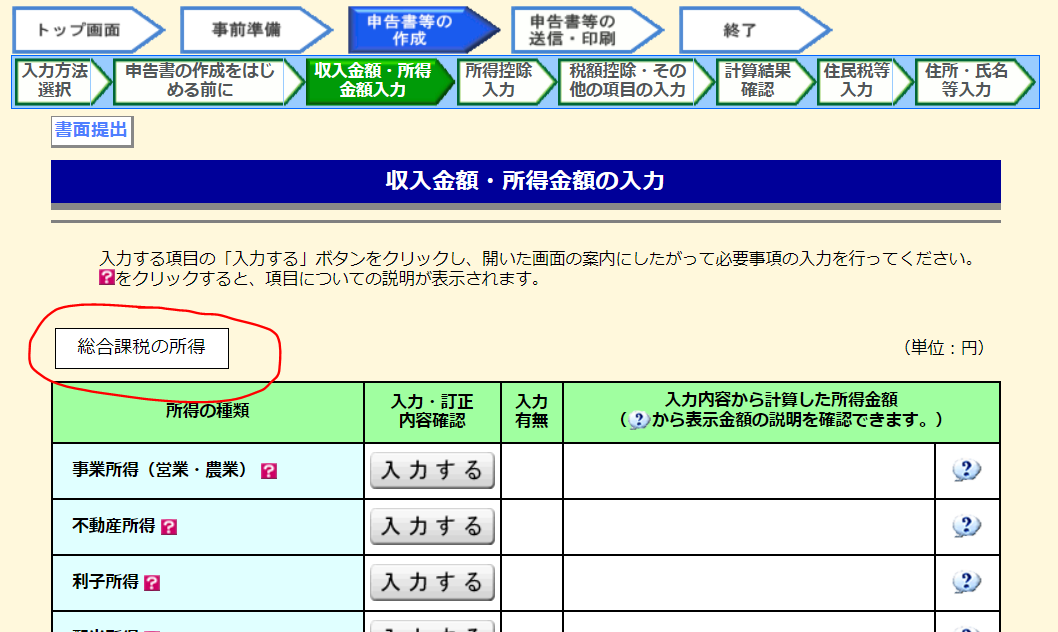

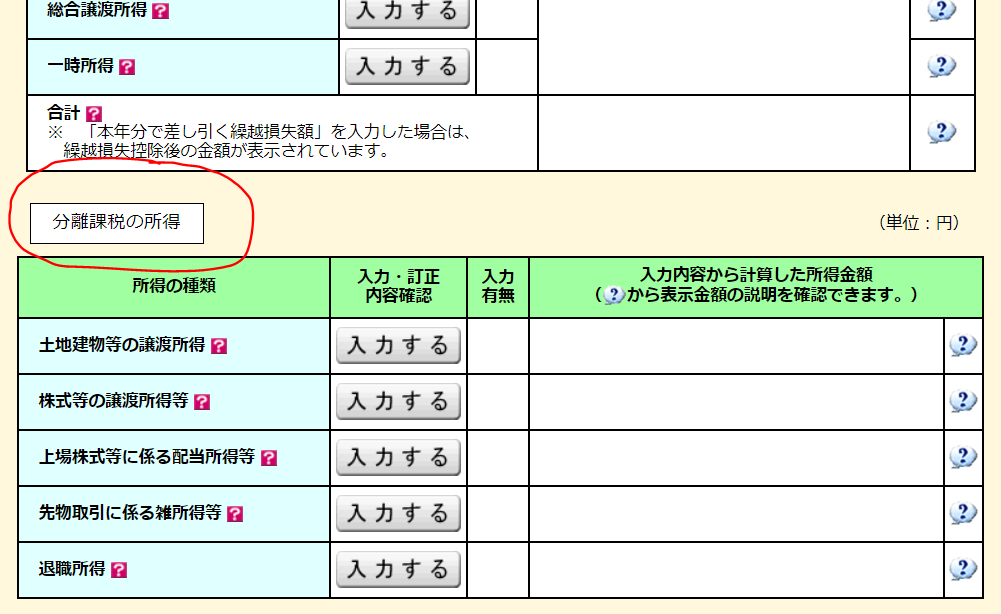

When you got to the page 「収入金額・所得金額の入力」 you’ll find two tables, separated by 「総合課税の所得」 and 「分離課税の所得」.

Table under 「総合課税の所得」 is used for inserting tax relating to Comprehensive taxation.

Table under 「分離課税の所得」 is used for inserting tax relating to Separate taxation.

Insert your incomes to appropriate fields by pressing on 「入力する」 button.

Example on how to Navigate:

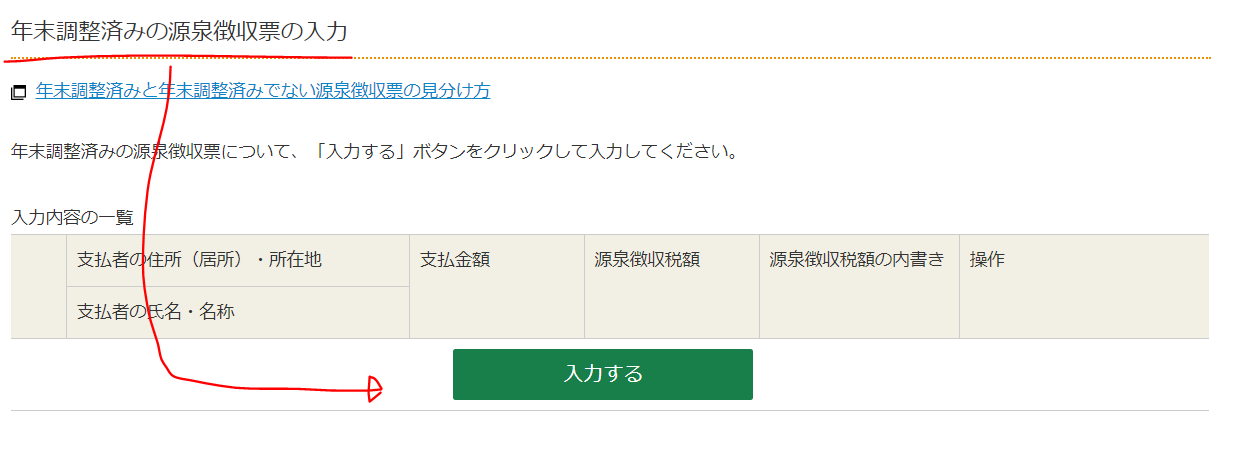

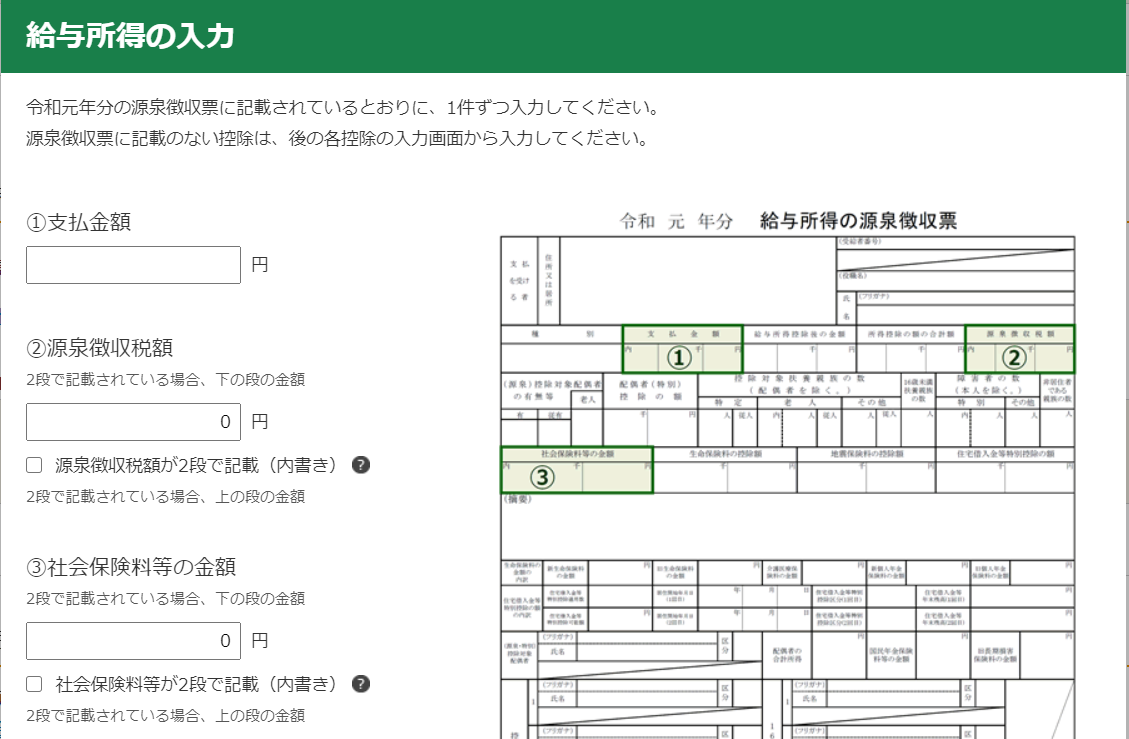

総合課税の所得 -> 給与所得 -> 年末調整済みの源泉徴収票の入力

Here you will, for example, insert income from your Company by using detail in your (gensen-choushuu-hyou) 源泉徴収票.

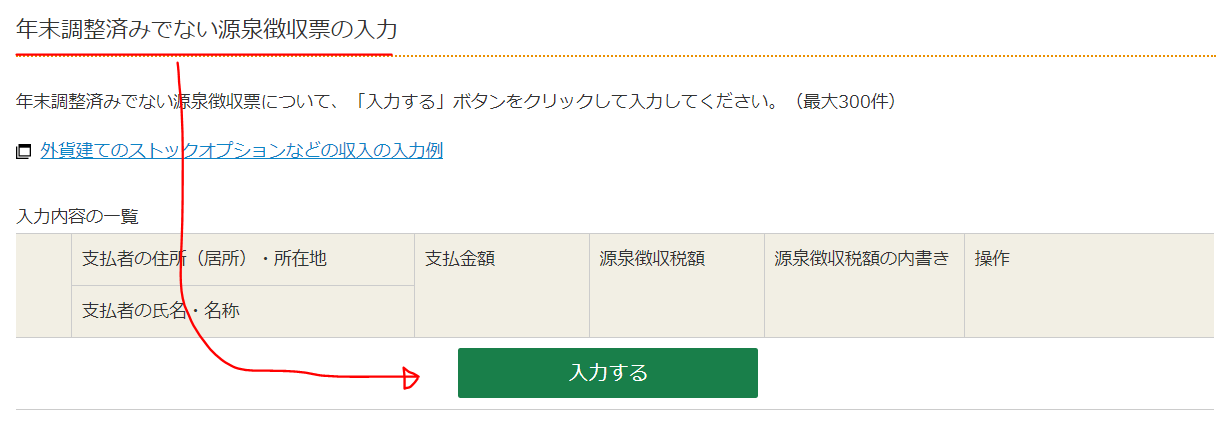

総合課税の所得 -> 給与所得 -> 年末調整済みでない源泉徴収票の入力

Here you will, for example, insert following incomes:

- ESPP Discounted Purchase

- RSU Discounted Purchase

Insert your calculated value to ①.

② and ③ will be 0.

Insert your company detail to 「支払い者」.

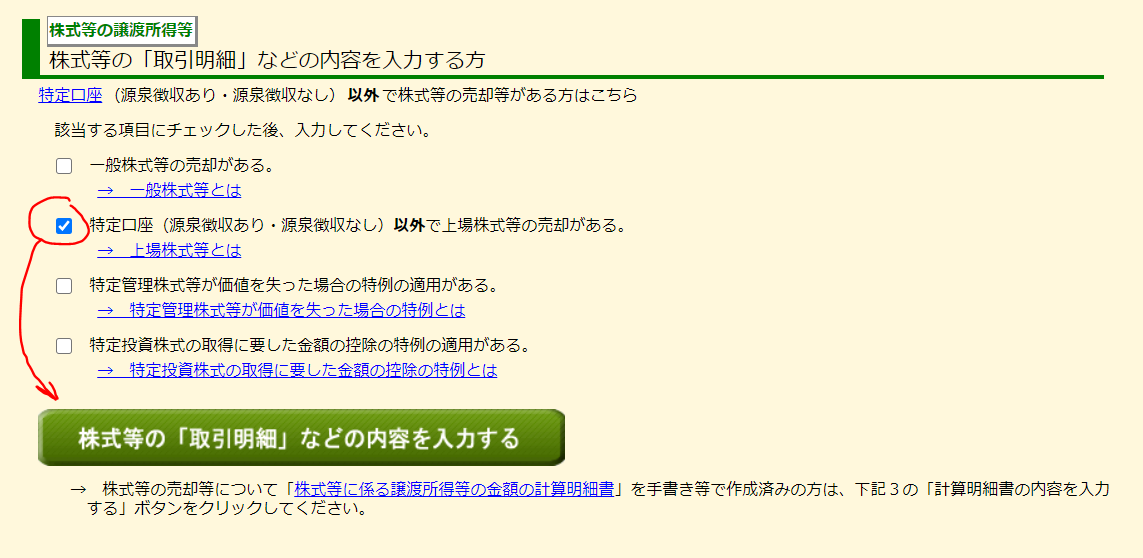

分離課税の所得 -> 株式等の譲渡所得等

Here you will, for example, insert following incomes:

- ESPP Share Sold

- RSU Share Sold

You will find below section as you scroll down. Enable checkbox 「特定口座(源泉徴収あり・源泉徴収なし)以外で上場株式等の売却がある。」 and click on green button.

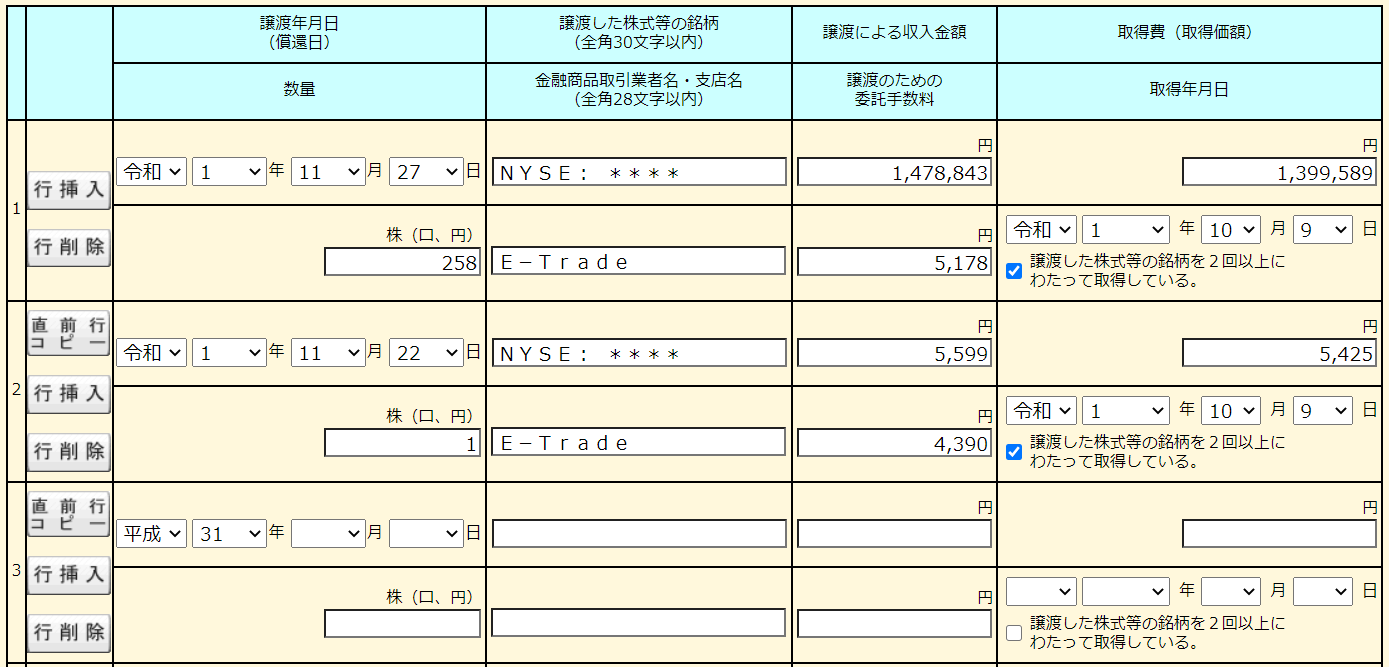

If I insert the incomes from above examples (ESPP Share Sold and RSU Share Sold), it will look like below.

As you can see from above, I’ve inserted stock symbol (ticker symbol) to 「譲渡した株式等の銘柄」.

Decimal places can be either floor’ed, ceil’ed or rounded. Choose the most beneficial one.

Now notice that “Acquisition Cost” do not match to one in examples. This is because I am using the Average Acquisition Unit Cost.

Below chart shows information regarding acquisition for sold share.

| Acquired Date | 9/10/2019 | 10/12/2018 |

|---|---|---|

| Type | RSU | ESPP |

| Quantity (Qty) | 12 | 258 |

| Acquired Date Market Value (MV) | 47 | 50 |

| Acquired Date TTS | 108.45 | 108.8 |

| Acquisition Cost $ (Qty * MV) | 564 | 12900 |

| Acquisition Cost ¥ ($ * TTS) | 61165.8 | 1403520 |

Using these values, “Average Acquisition Unit Cost” will be as below:

Then we multiply the sold share quantity to calculate the Acquisition Cost to insert to Kakutei-Shinkoku:

5424.762222 * RSU Share Sold (1) = 5424.762222

配当所得

Here you will, for example, insert following incomes:

- ESPP Dividend

- RSU Dividend

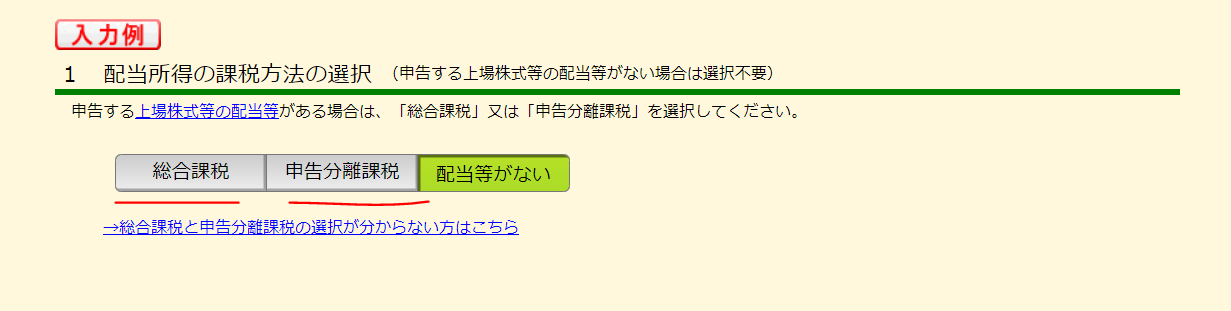

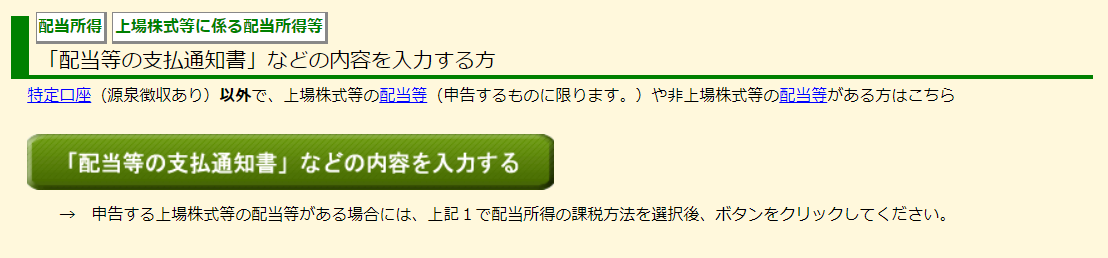

To insert Dividend info, navigate to 「総合課税の所得 -> 配当所得」 or 「分離課税の所得 -> 上場株式等に係る配当所得等」.

Both will take you to same page.

“Comprehensive taxation” or “Separate taxation” can be selected at 「配当所得の課税方法の選択」.

After selecting “Comprehensive taxation” or “Separate taxation”, scroll to middle of page and find following section. Click on the green button:

In the opened page, you will find two 「入力する」 buttons.

If you are declaring for Listed Stock, click on the 「入力する」 button at top.

If you are NOT declaring for Listed Stock, click on the 「入力する」 button at the bottom.

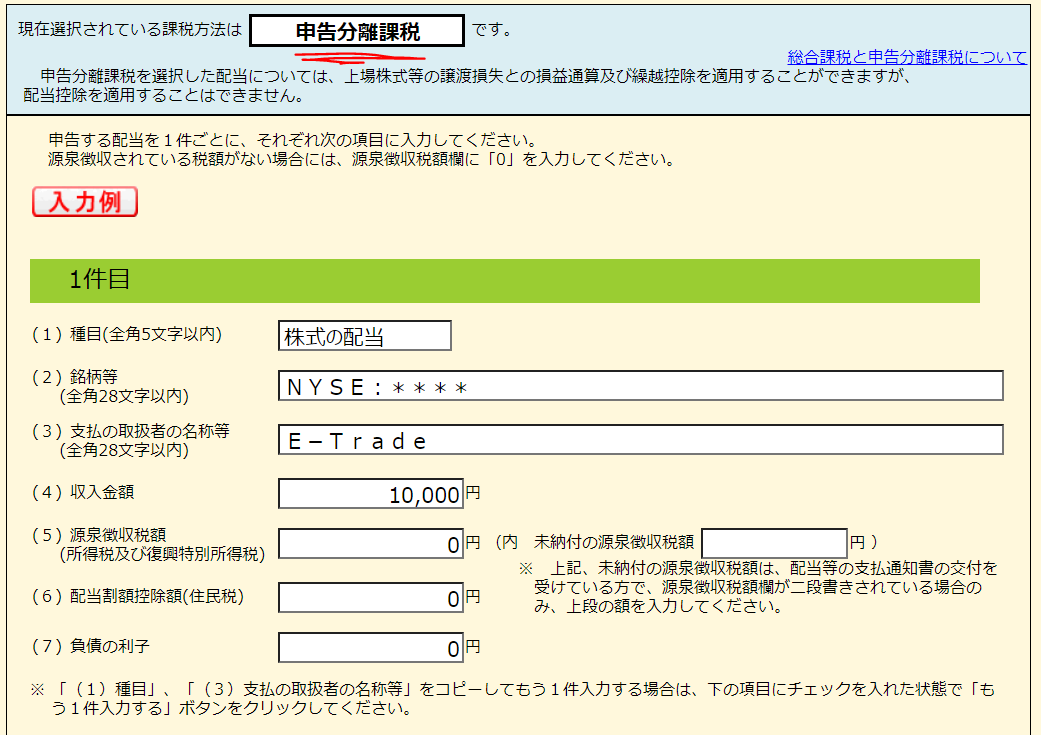

You will be taken to below screen when you’ve selected “Separate taxation” (「申告分離課税」) and clicked on 「入力する」 button for Listed Stock (one at top).

For ①, insert “株式の配当”

For ②, insert ticker symbol

For ③, insert Broker name

For ④, insert amount of dividend income you’ve received

0 for the rest.

分離課税の場合 -> 先物取引に係る雑所得等

Here you will, for example, insert following incomes:

- FX

Other References

https://mytips.hatenablog.com/entry/2020/02/17/131845

https://www.smbcnikko.co.jp/service/tax_sys/other/case01/index.html

Please let me know over comment below for any corrections.